Thursday July 9, 2015

The Business of Risk

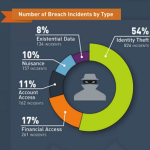

Cyber threats have created an interesting conundrum in which the criminal perpetrators are frequently more tech savvy than those responsible for preventing their crimes or apprehending them. And the situation, at the moment, doesn’t really show signs of improving.

Several national security experts recently issued recommendations to help address the problem. They referred to the issue as a “black elephant — a dangerous crossbreed between the ‘black swan’ risk (capable of producing unexpected outcomes with enormous consequences) and the ‘elephant in the room’ (a large problem that is in plain sight).”

[CLICK HERE to read the article, “We Don’t Need a Crisis to Act Unitedly Against Cyber Threats,” from Knowledge@Wharton, June 1, 2015.]

[CLICK HERE to read the article, “RSA Conference: Is Hiring Hackers a New Thing?” from Adeptis Group, May 6, 2015.]

[CLICK HERE to read the article, “Security Companies Hire Hackers, Ex-Spies to Fight Cyber Attacks,” from Bloomberg, April 14, 2015.]

While hackers certainly present a grave risk at the national level, frequently the outcomes are more personal. Sure, it’s a real blow to companies like Target and Home Depot for their data to be hacked, but ultimately it’s their customers who may suffer more relative damage.

And as great as technology is, the more we integrate it into our lives, the more risk we face of being personally “hacked.” For example, what a wonderful convenience to be able to lock and unlock our homes and cars using our cellphones, even when we’re out of town. But consider the benefit to a criminal who hacks into a person’s phone and unlocks the house and car, making for easy theft while knowing the owner isn’t home. It kind of makes the old-school, trusty German shepherd seem a bit more attractive for warding off potential burglars.

[CLICK HERE to read the article, “Data breaches may cost less than the security to prevent them,” from TechRepublic, April 9, 2015.]

[CLICK HERE to read the article, “Black Hat 2014: Security experts hack home alarms, smart cars and more,” from CBS News, Aug. 6, 2014.]

Then there are the security breaches that don’t make the headlines. For example, a data breach at a local vendor that results in unauthorized charges to your bank debit card, PayPal account or other online vendor. These sporadic incidents can range in damages from a minor inconvenience to lost hours trying to identify the issue, resolve it and get your money reimbursed.

Naturally, it makes sense to protect your own data as much as possible instead of relying solely on vendor and government solutions. For example, experts recommend using a credit card instead of a debit card. Relevant to this advice, it’s a good idea to revisit any of your accounts where you may have entered your bank account or debit card information, even if you only use your credit card with those accounts. Consider what card information is stored at accounts such as Amazon, eBay, Etsy, PayPal, Netflix and other online merchants you might frequent.

And with another nod to the old-school approach, consider using cash instead of credit at places where they habitually take your credit card out of sight for a few moments (long enough to record its information) — such as at restaurants and fast-food joints.

[CLICK HERE to read the article, “7 Reasons Your Debit Card Makes You a Target for Fraud,” from MagnifyMoney.com, Oct. 22, 2014.]

[CLICK HERE to read the article, “New ways to prevent credit-card fraud,” from Consumer Reports, May 28, 2015.]

One thing we’ve learned throughout history, no matter the threat, is that the best time to prepare for a disaster is before it occurs. This applies not only to cyber threats, but to health care screenings and creating a plan for retirement security. The more we educate ourselves and the more we plan, the more prepared we are when something unexpected occurs.

We are here to help you feel more confident in your financial strategy — now and in the future. Please give us a call at 770-778-5242 or at: wctucker@thewoodvillegroupllc.com.

We are an independent firm helping individuals create retirement strategies using a variety of investment strategies and products to custom suit their needs and objectives.

This content is provided for informational purposes only. It is provided by third parties and has been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. If you are unable to access any of the news articles and sources through the links provided in this text, please contact us to request a copy of the desired reference.